From job data missing the market and affecting the USD and Treasury Bond Yields to the FOMC meeting recap, read on to get the latest market analysis and news.

Private Job Data Proves Expectations Wrong

The ADP private employment figure was published yesterday and came well below what the market expected – 107,000 added workers versus the 145,000 expected.

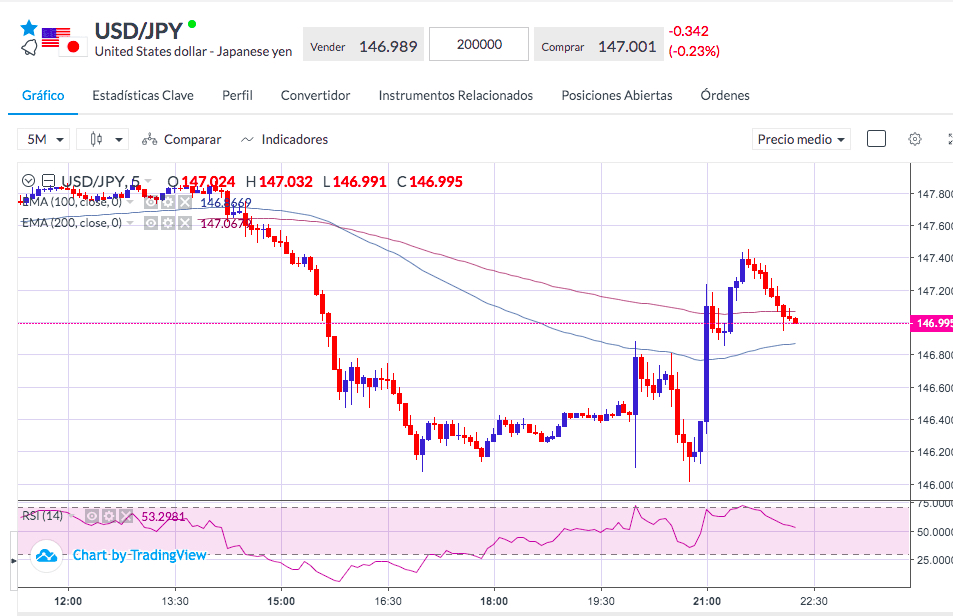

This caused the market to react with Treasury Bond Yields (market interest rates) falling. The 2-year bond lost more than 10 bps and the US Dollar weakened, especially in the USD/JPY pair which fell more than 150 pips. Stock index futures recovered some losses that occurred before the start of the session.

USD/JPY 5-minute chart, January 31, 2024. Source: MarketsADV WebTrader.

The prospect of a weaker labor market, especially before the initial employment data, Nonfarm Payrolls, which will be released tomorrow, encouraged investors to think that the Federal Reserve would be closer to the beginning of rate cuts than are planned for this year. But the outcome of the Federal Reserve meeting that took place a few hours later was not so optimistic in this regard.

FOMC Meeting Recap Pushes Off the Notion of Lowering Interest Rates

The report of the meeting stated that the Committee does not consider it appropriate to reduce the Federal Funds Rate until greater confidence has been gained that inflation is moving sustainably toward 2%.

Inflation figures have moved in the right direction in the last 6 months and are approaching the target level of 2%, so this phrase in the statement was shocking for the market and all previous movements were reversed with the Dollar strengthening, stock markets falling, and market rates rising.

Powell’s Statements Sway the Markets

It can be noted that Powell has recently earned a reputation for making comments during the news conference that are more moderate, and in some cases, differ from those in the meeting report.

With that, Powell, in response to a question, said that almost everyone on the Committee believes lowering rates is appropriate and that an unexpected drop in unemployment would “absolutely” argue in favor of cutting rates sooner. With these two clearly “dovish” comments, the market perked up again and stock indices turned positive again.

But the joy was short-lived and another comment saying that he does not believe it is likely that the committee will reach a sufficient level of confidence to lower rates in March was enough to bring pessimism back to the market.

In short, a high volatility session full of indecision due to Powell’s somewhat contradictory comments.

Basically, all that is clear is that interest rates will have to go down this year and that a somewhat lower inflation figure or employment data, like tomorrow’s Friday, that shows a weakening of the employment market, could speed up this decision.

Big Apple to Report Earnings Today

Lastly, investors await the largest market cap company in the world to report today, Apple (AAPL). With an earnings per share forecast around $2.09, traders should keep an eye on potential market movements in the stock and relevant indices.

Key Takeaways

- Job data came in much lower than expected.

- Treasury Bond Yields fell in response with the 2-year bond losing more than 10 bps.

- The USD in response rose. Boosting the USD/JPY pair.

- Powell statements swing, but all-in-all the decision to interest rates are not planned until it is closer to 2%.

- The NFP release is tomorrow. Traders await more clarity as it could give more information on rate changes.

- Investors await the biggest market cap company worldwide to report today, Apple.